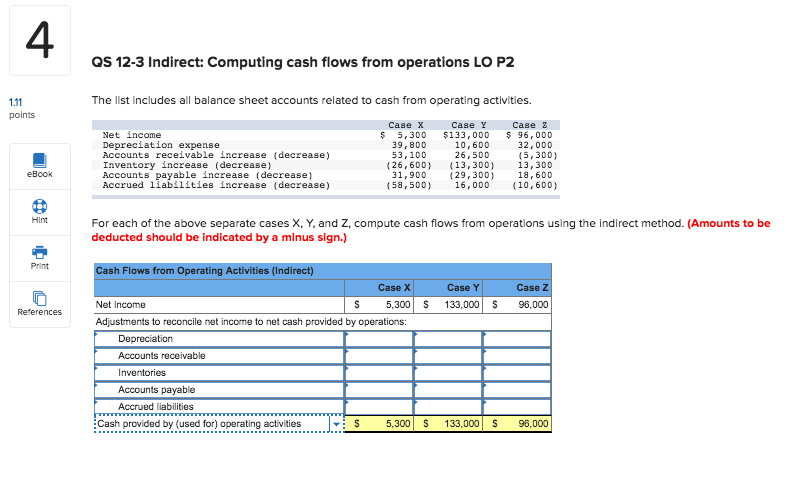

As a rule, a reduced DTI proportion is the best if you’re making an application for a good financial. Yet , certain DTI standards can differ according to home loan system and you can lender you are using to secure investment for your house pick.

DTI requirements having FHA loans

But really you should understand that not absolutely all lenders is actually willing to do business with consumers who’ve high DTI ratios. Loan providers normally set their unique individual standards where DTI percentages (or other loan standards) are concerned.

Particular loan providers may undertake FHA financing individuals having DTI rates while the highest as the 57%. Other lenders may lay the new DTI limits to have individuals within a great far lower height-often around 40% instead.

DTI requirements getting Virtual assistant funds

Va funds can be a fees-efficient way for qualified energetic-obligation armed forces services users, accredited pros, and you will thriving partners being people. Just do Virtual assistant funds bring eligible consumers the chance to pick a property without downpayment requisite, Virtual assistant finance also provide alot more easy DTI requirements in contrast to almost every other brand of mortgage loans.

Which have Virtual assistant loans, there is no limitation DTI ratio maximum. Yet individual loan providers try free to set their particular guidelines. You will need to talk to your own financial to determine what DTI proportion standards you really need to fulfill for people who get good Va mortgage. And it is important to review your finances to make sure you do not overcommit oneself economically possibly.

DTI criteria for USDA loans

USDA finance try an alternate government-supported real estate loan program getting reduced- and you can moderate-income borrowers who would like to get house inside the eligible rural elements. As a whole, you want a good DTI proportion regarding 41% or straight down as entitled to a beneficial USDA financing.

Such sensible loans including feature zero deposit without minimal credit rating conditions. But personal loan providers commonly favor consumers to possess a good 620 FICO Rating or more.

Just how to improve your DTI proportion

Cutting your financial obligation-to-income ratio before you apply having home financing could possibly get alter your odds of qualifying to own a mortgage (and getting a diminished interest rate). Here are some ideas that could help you lower your DTI ratio.

- Reduce loans. Envision paying off personal debt prior to their mortgage application as much as possible afford to do it. As you reduce the stability you borrowed so you’re able to creditors towards the certain expenses, eg playing cards, their DTI ratio get reduction in effect. Plus, for many who work with paying credit debt, you could take advantage of the amazing benefits of enhancing your credit rating and you may spending less on the charge card desire charge also.

- Improve earnings. Earning extra cash is another possible answer to change your DTI ratio. But it’s vital that you just remember that , this plan is almost certainly not a magic pill where the financial software is concerned. Taking a boost at the office could well be helpful when your company try willing to give a page proclaiming that money improve was long lasting. But when you pick-up part-date work to earn more funds, possible usually you desire no less than several years’ worth of tax statements one to show you’ve been making that cash several times a day prior to the lender have a tendency to count them for DTI calculation purposes.

- Put a beneficial cosigner or co-debtor. The brand new improvement listed here is whether the other individual has entry to the cash you’re credit. Otherwise, they truly are good cosigner. Whenever they perform, these include a good co-debtor. In any event, they might be agreeing to invest right back the mortgage if you standard. click to read Adding an effective cosigner otherwise co-debtor may slow down the full DTI ratio on your mortgage in the event that they earn additional earnings and you will owe a lot fewer bills as compared to your. And you will, while implementing with a wife or companion, you’ll be able to intend to include these to the borrowed funds anyway. But be aware that if a cosigner’s DTI ratio was highest than yours (or similar), adding these to the application may possibly not be since useful given that might guarantee.